KEY HIGHLIGHTS

- Singapore’s Retirement Payout Planner helps you forecast lifelong CPF LIFE payouts from 2026 onwards

- Small changes like delaying payouts or topping up CPF can raise monthly income more than most expect

- Best used together with SRS and Silver Support for a realistic retirement cashflow plan

Thinking about retirement in Singapore usually triggers one big question: how much will I actually get every month?

That’s where the Retirement Payout Planner comes in. For 2026, it remains one of the most useful CPF tools to help Singaporeans estimate lifelong payouts — especially when paired with the Monthly Payout Estimator.

The planner isn’t just about numbers. It helps you see how choices like when you start payouts, how much you top up, and which CPF LIFE plan you pick affect your monthly income for the rest of your life. For most Singaporeans, this clarity is more important than chasing perfect returns.

Right after you understand the basics, it helps to compare the tools available and know when to use which one.

| Tool | What It Does | Best For |

|---|---|---|

| Retirement Payout Planner | Lets you test multiple scenarios: payout age, top-ups, CPF LIFE plans, SRS income | Long-term planning and “what-if” analysis |

| Monthly Payout Estimator | Gives a fast estimate based on current CPF balances and start age | Quick checks and single-scenario estimates |

Why the Retirement Payout Planner Matters More Than Ever in 2026

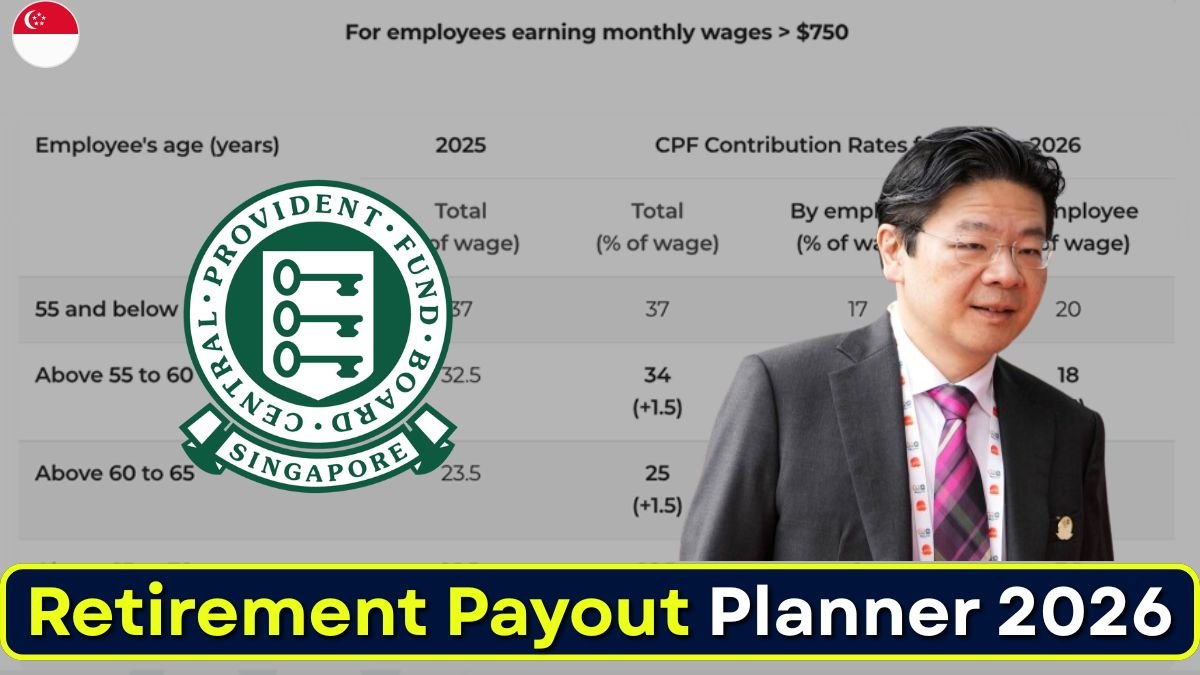

Singapore’s retirement system still revolves around CPF LIFE and your Retirement Account (RA). But retirement sums rise every year, and even a 1–2 year delay in payouts can significantly boost monthly income. The planner shows this clearly, without guesswork.

For 2026, the Basic Retirement Sum (BRS), Full Retirement Sum (FRS) and Enhanced Retirement Sum (ERS) continue to be adjusted annually. These benchmarks are not random — they directly influence how much CPF LIFE pays you every month. If you don’t plan around them, you’re basically flying blind.

Key Singapore Retirement Building Blocks (2026)

CPF LIFE and Retirement Sums

CPF LIFE is a lifelong monthly payout scheme. The amount you receive depends mainly on how much is in your Retirement Account at age 55 and when you start payouts (from age 65 to 70).

The three retirement sums — BRS, FRS and ERS — act as planning targets. You don’t need to hit ERS to retire, but higher sums generally mean higher lifelong payouts. The planner lets you see the trade-offs clearly, no need to overthink.

Supplementary Retirement Scheme (SRS)

SRS remains one of the most underused tools in Singapore. Contributions give immediate tax relief, and investment gains are tax-deferred. The key detail most people miss: only 50% of SRS withdrawals are taxable if withdrawn after the prescribed retirement age.

Used properly, SRS helps bridge early retirement years or top up CPF LIFE payouts later — especially useful for higher-income earners today.

Silver Support Scheme

Silver Support provides quarterly cash payouts to eligible lower-income seniors aged 65 and above. There’s no need to apply — assessment is automatic. Amounts depend on lifetime CPF contributions, household income per person, and housing type.

Even if payouts are modest, they form a reliable “floor income” and should always be included in conservative retirement planning.

How to Use the Retirement Payout Planner (Step-by-Step)

Start by gathering your numbers. You’ll need your CPF OA, SA and MediSave balances, your current SRS balance, and a rough idea of monthly retirement expenses in S$.

Begin with the Monthly Payout Estimator to get a baseline figure. Once you’re comfortable, move to the Retirement Payout Planner to test variations — delaying payouts, topping up RA, or switching CPF LIFE plans.

Create at least three scenarios:

- Conservative: No top-ups, payouts start at 65

- Balanced: Top up to BRS or FRS, payouts start at 67

- Aggressive: Top up to ERS, payouts delayed to 70

Then layer in SRS withdrawals and stress-test your plan against medical costs or market downturns. If your base plan still works, you’re on the right track.

Realistic Examples (Simplified)

Example 1: Ms Tan, age 54

Her RA is projected to have S$120,000 at 55. Starting CPF LIFE payouts at 65 under the Standard Plan gives an estimated ~S$1,200/month. By adding S$400/month from SRS withdrawals, her total income reaches ~S$1,600/month.

Example 2: Mr Lee, age 45

He plans to top up gradually to the FRS by 55 and delay payouts to 67. The planner shows a noticeable increase in monthly CPF LIFE payouts compared to starting earlier — enough to justify the wait for him.

(Actual payouts depend on individual CPF records. Always confirm with the official estimator.)

Practical Ways to Boost Your Monthly Retirement Income

Topping up your Retirement Account at or after 55 has one of the biggest long-term impacts on payouts. If liquidity allows, it’s often more effective than chasing higher-risk investments.

SRS works best when your current tax rate is higher than what you expect in retirement. Delaying CPF LIFE payouts, even slightly, also increases monthly income — something many Singaporeans underestimate.

Most importantly, keep emergency cash outside CPF. CPF is reliable, but it’s not flexible.

Frequently Asked Questions

1. Should I use the Retirement Payout Planner or the Monthly Payout Estimator?

Use both. The estimator gives fast numbers; the planner helps you make strategic decisions across multiple scenarios.

2. Can I access my CPF savings before age 55?

Generally no. CPF is meant for retirement, with only limited exceptions such as medical needs.

3. Is SRS withdrawal fully taxable in retirement?

No. If withdrawn after the prescribed retirement age, only 50% of the amount is taxable, subject to current rules.

Sources & where to run the numbers (official tools)

- CPF LIFE — CPF monthly payouts and plans. Central Provident Fund

- CPF Monthly Payout Estimator & Retirement Payout Planner. Use these official online tools to produce personalised payout estimates. Central Provident Fund

- Retirement Sums (BRS/FRS/ERS) and official CPF guidance. Central Provident Fund+1

- SRS tax rules — IRAS. Default

- Silver Support Scheme — CPF/MOM pages for eligibility and payment tiers. Central Provident Fund+1