KEY HIGHLIGHTS

- Short-term FD promos in Singapore are still paying around 1.30%–1.35% p.a. as we head into 2026.

- Most higher rates require fresh funds and online placement.

- For most Singapore savers, short tenures + promo hopping make more sense than locking long-term.

Thinking of parking your cash in a fixed deposit in 2026? You’re not alone. With market uncertainty still around and savings account rates cooling, many Singaporeans are asking the same question: FD still worth it or not?

Rates aren’t climbing aggressively anymore, so the real gains come from picking the right bank, the right tenure, and the right promo.

Here’s a clear, no-nonsense breakdown for Singapore savers — whether you’re managing emergency funds or just letting idle cash work harder.

After the rate spikes of previous years, the landscape has shifted. Following policy easing in 2025, banks are now more selective, using targeted promotions instead of across-the-board hikes. That’s why comparing deals matters more than ever in 2026.

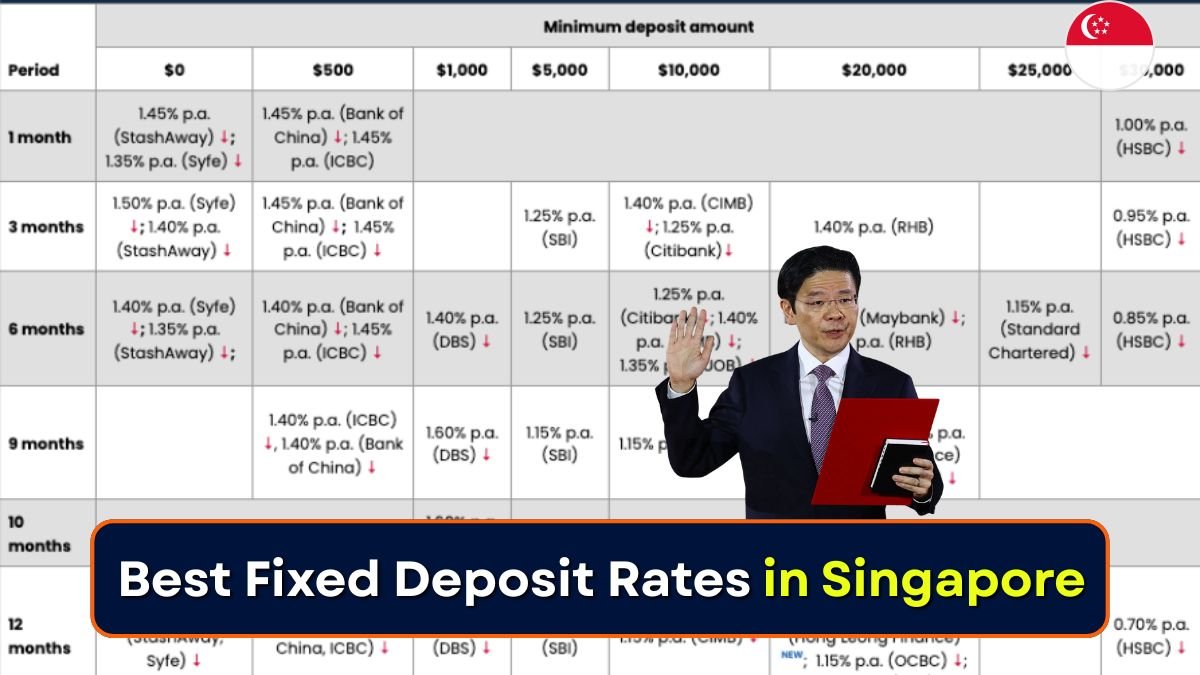

Fixed Deposit Promos in Singapore

| Bank / Provider | Typical Promo Tenure | Promo Rate (p.a.) | Minimum Deposit |

|---|---|---|---|

| CIMB Singapore | 3, 6, 12 months | 1.30%–1.35% (online) | S$10,000 |

| Maybank Singapore | 6, 12 months | ~1.30% (6m promo) | S$20,000 |

| UOB | 6 months (fresh funds) | ~1.20% | S$10,000 |

| OCBC | 9, 12 months | ~1.15% | S$20,000 |

| HSBC Singapore | 1–12 months | Varies (some promos higher) | Varies |

| Other banks (ICBC, RHB, SCB) | Short tenures | 1.10%–1.40% | Varies |

Rates change fast. Always confirm on the bank’s official site before placing funds.

Why Fixed Deposits Still Matter in 2026

For most Singaporeans, fixed deposits remain one of the lowest-risk ways to earn predictable returns on SGD savings. You won’t get rich, but you also won’t lose sleep.

The key difference versus savings accounts? Certainty. You know exactly how much interest you’ll earn, as long as you don’t break the FD early.

In 2026, the smart move isn’t chasing the longest tenure — it’s using short-term promos strategically.

How to Choose the Right Fixed Deposit (Singapore Context)

Match the tenure to your cash needs

If this is emergency or near-term money, stick to 1–3 months or use laddering. Parking funds you won’t touch? 6–12 months may pay slightly better, but the difference isn’t huge.

Fresh funds matter — a lot

Most attractive promos require fresh funds, meaning money not currently held with that bank. Moving funds via FAST between banks is usually enough, but always read the fine print.

Don’t miss the minimum deposit

Many promos only apply if you place S$10,000 or S$20,000. Miss it by even a dollar, and you may drop to a much lower base rate.

Understand how interest is paid

Check whether the rate shown is nominal or effective interest rate (EIR). Also confirm if interest is paid only at maturity — most FDs work this way in Singapore.

Early withdrawal penalties are real

Break an FD early, and you’ll usually lose most or all interest. If liquidity matters, shorter tenures are safer. No need to overthink this one.

Laddering is still your friend

Split funds into multiple FDs with staggered maturities. This keeps some cash maturing every few months, giving you flexibility to grab new promos.

Tax Treatment, What Singapore Savers Should Know

For individuals, interest earned on SGD bank deposits is generally not taxed under Singapore’s current framework. There’s no capital gains tax here. Still, if you’re placing large sums or have special circumstances, it’s wise to double-check with IRAS or a tax professional.

FD Rate Outlook for 2026

With inflation cooling and policy remaining accommodative, banks are unlikely to raise FD rates aggressively in early 2026. Instead, expect:

- Short, time-limited promos

- Online-only or fresh-funds-only deals

- Banks competing selectively for deposits

Honestly speaking, promo hunting beats loyalty in this environment.

Practical Checklist Before You Place an FD

- Confirm promo start and end dates

- Check if online application is required

- Ensure you meet the fresh funds rule

- Note the maturity date and auto-renewal terms

- Compare effective returns, not just headline rates

Example FD Strategies That Make Sense in 2026

Conservative: 6-Month Ladder

Split funds across two or three banks with staggered 6-month FDs. Good balance between yield and flexibility.

Opportunistic: Short-Term Promos

Jump on 3-month online promos, then rotate funds when better deals appear. Best for hands-on savers.

Set-and-Forget: 12-Month FD

Only worth it if you secure a genuinely competitive rate and won’t need the money. Less admin, less flexibility.

Frequently Asked Questions

Are fixed deposit interest earnings taxable in Singapore?

For most individual savers, SGD FD interest is not taxed. If your situation is complex or business-related, check with IRAS or a tax advisor.

Is it better to choose a 3-month or 12-month FD in 2026?

For most Singaporeans, shorter tenures make more sense in 2026 due to uncertain rate direction and frequent promos.

Do online or digital placements really pay more?

Yes. Many banks reserve their best FD rates for online or fresh-fund placements, so always check the channel conditions.